Regulatory Compliance for Your Financial Consulting Website on Squarespace

Key Takeaways Regulatory Compliance for Your Financial Consulting Website on Squarespace

FCA Handbook rules on financial promotion apply to website content describing financial services

Financial promotion rules require clarity on regulated status, restrictions on return claims, and risk warnings

GDPR applies to all prospect data collected via your website contact forms

Professional standards (ICAEW, CIMA, FPA) impose additional ethical requirements beyond legal minimums

Unregulated consultants face different requirements than FCA-regulated advisors

Regular compliance audits of website content prevent regulatory drift and ensure ongoing adherence

IMPORTANT DISCLAIMER: This guide provides general information about regulatory frameworks that may apply to financial consulting websites. It is not legal advice, not tailored to your specific situation, and does not constitute compliance guidance. Before implementing any website features, you must consult directly with your compliance officer, legal counsel, or the FCA. The responsibility for regulatory compliance rests entirely with you and your firm.

A financial consulting website on Squarespace must navigate complex regulatory requirements: FCA financial promotion rules, GDPR data handling for financial prospects, professional standards, and disclosure obligations. Unlike other business websites, financial advisory websites operate within tightly defined regulatory boundaries.

This guide provides a compliance framework and 20-item checklist for UK financial consulting websites. However, compliance requirements vary by whether your firm is FCA-regulated, an appointed representative, or unregulated. Consult your compliance advisor before implementing any changes based on this guide.

FCA Financial Promotion Rules

What Are Financial Promotion Rules?

The FCA's financial promotion rules (COBS 4.2R in the FCA Handbook) apply to communications about financial products or services. These rules affect financial consulting websites through multiple dimensions:

Scope: The rules apply if your website describes advisory services (M&A advisory, corporate restructuring, financial planning) in a way that could be seen as financial promotion—which includes virtually all financial consulting website content.

Key requirements:

Communications must be "fair, clear and not misleading"

Return claims (e.g., "typical returns") require specific disclaimers

Risk warnings must be included for services involving financial risk

Regulatory status (regulated, appointed representative, unregulated) must be clear

Financial crime references (sanctions compliance, AML) cannot be used as marketing claims

Regulated vs. Unregulated Consultants

FCA-regulated financial consultants (holding FCA permission for advisory services) face stricter promotion rules but can claim regulated status prominently.

Appointed representatives (working under an FCA-regulated principal firm) must clearly identify the regulated firm and principal.

Unregulated consultants face reduced legal compliance requirements but may still face professional standards obligations through professional bodies (ICAEW, CIMA, FPA).

The distinction fundamentally affects what your website can claim. Clarify your regulatory status with your compliance advisor before publishing any content.

Financial Promotion Principles

Communications must follow these FCA principles:

Fair: Not misleading through presentation or selectivity

Clear: Language appropriate for target audience (sophisticated vs. retail clients)

Not misleading: Including risks, limitations, and appropriate disclaimers

Practical examples:

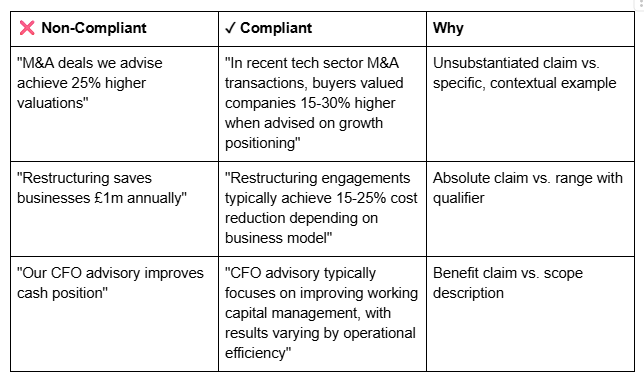

❌ "Restructuring can save businesses £50,000 annually" (unqualified benefit claim)

✓ "In cases similar to yours, restructured businesses typically achieved 20% cost reductions, though results vary" (qualified, contextualised)

❌ "Our M&A advisory delivers £2m average transaction value increases" (unsubstantiated performance claim)

✓ "We advise on M&A transactions averaging £5m-£50m transaction value across manufacturing and tech sectors" (factual scope description)

Required Website Disclosures

Regulatory Status Display

Every financial consulting website must clearly communicate regulatory status. This is not optional—it's a legal requirement if you're regulated and an ethical requirement if you're unregulated.

If FCA-regulated:

All pages should include status statement (typically in footer):

"We are authorised and regulated by the Financial Conduct Authority [Firm Reference Number: XXXXXX]. You can check our FCA status at the."

If appointed representative:

"[Your name] is an appointed representative of [Principal firm name] which is authorised and regulated by the FCA [Firm Reference Number: XXXXXX]."

If unregulated:

Depending on your professional body affiliation, you might state:

"We are not FCA-regulated. We are [ICAEW members/CIMA members/FPA members], bound by professional ethical standards."

Regulatory status should be on homepage (often in header or trust section) and footer of all pages.

Risk Warnings for Advisory Services

Services involving financial risk require appropriate risk warnings. The extent depends on service type:

M&A advisory: Include general risk warning that M&A transactions involve significant financial and operational risk, recommend thorough due diligence.

Restructuring advisory: Include warnings that restructuring may involve redundancies, asset sales, or other material changes; outcomes cannot be guaranteed.

Financial planning/FP&A advisory: Include warnings that financial forecasts involve inherent uncertainty; actual results may vary materially from projections.

Regulatory position: Risk warnings are primarily required for investment advisory or insurance mediation. For pure financial consulting on restructuring or M&A, risk warnings are advisable best practice, not strict legal requirements, but consult your compliance advisor.

Performance and Past Results Disclaimers

If you mention past client outcomes (case studies, testimonials, track record), include appropriate disclaimers:

"Past performance is not a reliable indicator of future results. All client engagements are unique, and outcomes depend on specific circumstances, client implementation, and market conditions."

This disclaimer should be visible near any performance claims or case studies.

Conflicts of Interest Disclosure

If your firm has potential conflicts (e.g., advisory on both buyer and seller side of M&A, fees structured in ways that could create incentives), disclose these on a dedicated page or section.

Example disclosure framework:

"We advise both buyers and sellers in M&A transactions. We manage conflicts through fee transparency and engagement scope clarity. Book a call is available on request."

GDPR and Data Handling

Website Form Data Collection

Every contact form, email signup, or data collection point on your Squarespace website must comply with GDPR:

Required elements:

Privacy notice: Clear statement of what data you collect and why

Consent mechanism: Explicit consent (checkbox) for data processing, separate from form submission

Data retention policy: Clear statement of how long data will be kept

Third-party sharing: Disclose if data is shared with CRM providers, email services, or consultants

Data subject rights: Statement of right to access, amend, delete personal data

Squarespace GDPR implementation:

Add GDPR consent checkbox to all contact forms

Link privacy notice from every form

Ensure email capture only uses double opt-in (initial signup + confirmation email)

Document data retention periods (recommend 12 months for inactive prospects, longer for clients)

Ensure Squarespace's terms comply with GDPR (they generally do, but verify)

Financial Data Privacy

If you collect sensitive financial data (revenue, profitability, shareholder structure) through your website, enhanced protections apply:

Ensure forms use HTTPS encryption (Squarespace provides this by default)

Minimise data collection (ask only what's necessary)

Include specific notice about financial data handling

Limit access to team members with need-to-know

Document secure storage and deletion procedures

Client Testimonials and Case Studies

Using client names, companies, or identifying information in testimonials requires explicit written consent. GDPR treats this as personal data processing:

Get written client consent before publishing testimonial with identifying details

Offer anonymity option (e.g., "Managing Director, Mid-Market Manufacturing")

Document consent in your records

Remove testimonials if client withdraws consent

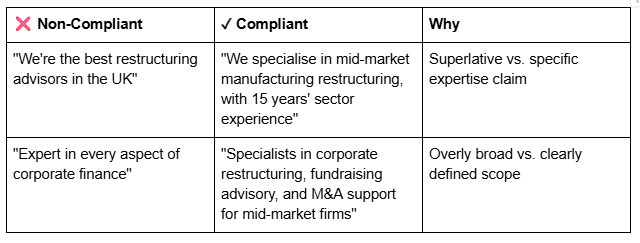

Financial Promotion Language Guide

The difference between compliant and non-compliant language is often subtle. This guide helps navigate common scenarios:

Claims About Results or Outcomes

Language on Expertise and Specialisation

Risk Communication

20-Item Compliance Checklist

Use this checklist to audit your Squarespace financial consulting website:

Regulatory Status (Items 1-3)

1. Regulatory status (FCA-regulated, appointed representative, or unregulated) clearly stated on homepage

2. FCA firm reference number displayed with link to FCA register (if regulated)

3. Regulatory status repeated in footer on all pages

Disclosures and Warnings (Items 4-8)

4. Risk warnings included for services involving financial risk or uncertainty

5. Past performance disclaimer displayed near all case studies and testimonials

6. Conflicts of interest policy available and linked from main pages if applicable

7. Engagement scope clearly defined (what is and isn't included in advisory)

8. Fee transparency (specific fees, ranges, or clear "contact for pricing" approach)

Professional Credentials and Standards (Items 9-11)

9. Team member credentials prominently displayed (CIMA, ICAEW, CFA, etc.)

10. Professional body memberships displayed with links to verification (ICAEW, CIMA, FPA)

11. Professional indemnity insurance information available (underwriter, cover limits, status)

Content and Language Compliance (Items 12-15)

12. No unqualified performance claims (all outcome claims include qualifiers or disclaimers)

13. Expertise claims limited to specific services and sectors where you have demonstrated capability

14. Client testimonials and case studies used only with explicit written consent

15. Testimonials use language clients actually used, not paraphrased or rewritten

Data Protection and Privacy (Items 16-18)

16. GDPR privacy notice linked from every contact form or data collection point

17. GDPR consent checkbox included on all lead capture forms

18. Data retention policy documented and disclosed to prospects

Technical and Governance (Items 19-20)

19. Website uses HTTPS (secure connection)—Squarespace provides this by default

20. Compliance audit process documented; website content reviewed quarterly for regulatory drift

Implementation note: Not all 20 items apply equally to every consultant. Regulated advisors must complete all items. Unregulated consultants may skip items 2 (FCA register) but must complete most others. Review this checklist with your compliance advisor to determine your specific requirements.

Professional Standards Beyond Legal Requirements

ICAEW Standards for Financial Consultants

If you're ICAEW-qualified, your website must reflect ICAEW's technical standards (TAGs) and ethical standards:

Competence: Claims must reflect actual expertise; no overstatement of capability

Integrity: Case studies and testimonials must be factual and representative

Professional conduct: Website tone must be professional, not aggressive or overstated

Confidentiality: Client case studies use only information clients permit disclosure of

CIMA Standards for Management Accountants

CIMA members must ensure websites comply with CIMA's Code of Ethics:

Integrity: All financial claims must be accurate and substantiated

Objectivity: Case studies must present balanced view of outcomes and limitations

Professional competence: Don't claim expertise outside actual qualification

Professional behaviour: Website tone should reflect CIMA's professional standards

FPA Standards for Financial Planners

If you're FPA-qualified, specific standards apply around financial planning claims and client suitability messaging.

Practical implication: Professional body membership creates additional compliance obligations beyond FCA legal requirements. Your professional body may have specific website standards. Consult your professional body's guidance before publishing major website changes.

Frequently Asked Questions

-

Yes, but with caution. Unregulated consultants must follow consumer protection laws (avoiding misleading marketing) and professional standards (if ICAEW/CIMA members). Testimonials must be factual, truthful, and represent typical outcomes. Avoid implying regulatory status you don't have.

-

Case studies can include specific metrics (cost reduction percentage, timeframe to resolution) if: (a) they're accurate and verifiable, (b) they include appropriate caveats ("in this case," "depending on circumstances"), and (c) they're not presented as typical or guaranteed outcomes. Include outcome range when possible.

-

Yes. GDPR applies to any personal data collection, including email addresses. You need: clear notice of why you're collecting the email, consent checkbox, and data retention statement. Squarespace forms should include GDPR elements.

-

Respect the client's preference. Use their feedback internally but don't publish identifying information without explicit consent. Many clients will consent if you request clearly and offer anonymity options.

-

Recommended practice is quarterly review (when you add case studies, testimonials, or service offerings). At minimum, annual review. Any major website redesign should trigger full compliance audit before publishing.

-

For FCA-regulated firms, non-compliance can trigger regulatory action, warning notices, or enforcement proceedings. For unregulated consultants, consequences include consumer complaints, professional body investigations (if member), and reputational damage. Prevention through regular compliance audits is essential.

Ensure compliance while building trust. Squareko builds Squarespace financial consulting websites that incorporate regulatory requirements as trust signals—FCA registration, credential displays, and risk warnings become confidence-builders rather than legal burdens.

From custom website design to SEO strategy, we help businesses launch a site that looks professional and performs better.

Author:

Walid Hassan, Squareko

I'm Walid Hasan, a Certified Squarespace Expert and Squarespace Circle Platinum Partner with over 12 years of hands-on experience designing and optimizing high-performing websites. Over the years, I've had the privilege of building more than 2,000 Squarespace websites for clients around the world, always focusing on clean design, strong user experience, and conversion-driven results.